A Quantitative Analysis of Aping Into A Twitter Wager

This research piece was written as a part of Paradigm's blog series to showcase insights pertaining to the cryptocurrency options market.

Within the crypto space it’s common to see people fight on Twitter over silly things. In many cases these arguments are a complete waste of time, however, in rare circumstances they present a unique opportunity for individuals to further reinforce their ideas by making public wagers.

A few weeks ago Sensei Algod, an anonymous crypto trader, stirred up some controversy on crypto Twitter by presenting arguments against UST citing it as an “unsustainable ponzi”. To spice things up further, Algod decided to offer a $1M bet that LUNA would be trading lower than the current price a year from now. As a result, Do Kwon, the founder of Terraform Labs, decided to take the other side of this bet. Shortly after several other Twitter profiles also entered the bet with popular crypto personality Cobie setting up a multisig wallet for storing the escrowed funds for the bet which can be viewed here.

The goal of this research is to analyze the structure of this bet and how to think about pricing exposures for Algod and Do Kwon. This piece will be broken down into several parts:

- Specifics of the bet and understanding payoff structures

- Evaluating the bet through options pricing

- Backtesting P&L of systematically trading LUNA binary options

- Thoughts on the future of the bet

1. Overview of The Bet

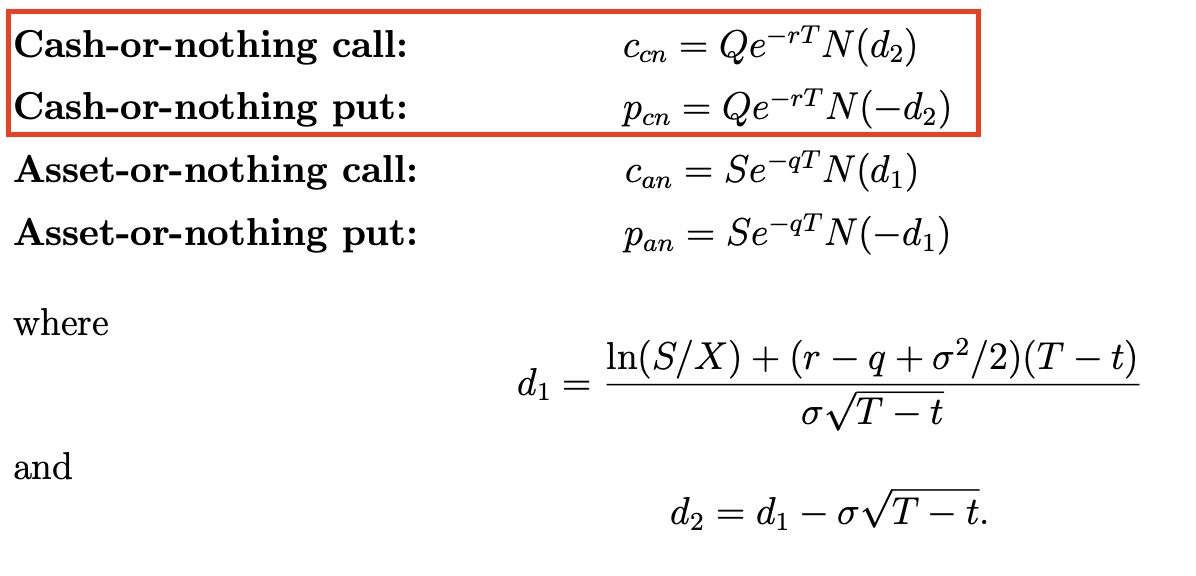

This payoff structure resembles a binary option in which the final result will depend entirely on the price of LUNA at expiration. While binary options are fairly new to crypto, they are actively traded in traditional finance mostly within the FX derivatives market. With this wager, we can think of the bet between Algod and Do as a cash-or-nothing binary option which offers a fixed payout depending on where LUNA is trading at expiration.

Let’s review the exposures for each party in this trade. At the time of the bet LUNA was trading around $88, therefore, we can use this as the strike price which can serve as a benchmark for determining whether LUNA is higher or lower a year from now. Furthermore, this bet was set up as a 50/50 bet with equal cash payouts in either scenario of LUNA being above or below $88 at expiration.

- Do Kwon is effectively long a 1 Year LUNA $88 Strike Binary Call Option which will pay $1M if LUNA greater than $88 by March 13, 2023

- Algod is effectively long a 1 Year LUNA $88 Strike Binary Put Option which will pay $1M if LUNA is less than $88 by March 13, 2023

2. Overview of Binary Options and Pricing:

For those familiar with vanilla options under standard Black-Scholes, the formula for binary options pricing will be very similar. In the case of a binary call option, we can generalize and think of N(d2) as the probability of the spot price being greater than strike at maturity and thereby use this to calculate the expected value of the fixed cash payout. A similar approach can be used for determining the fair value of the binary put option.

Similar to vanilla options trading, volatility is the most important variable when pricing out binary options. In the case of this bet, the market already knows the strike price ($88), spot price ($88), time to maturity (1 year) and expected cash payout ($1M USD). For interest rates we can take the median annualized funding rate for LUNA perpetual futures contracts over the past year on FTX which amounts to roughly +1%.

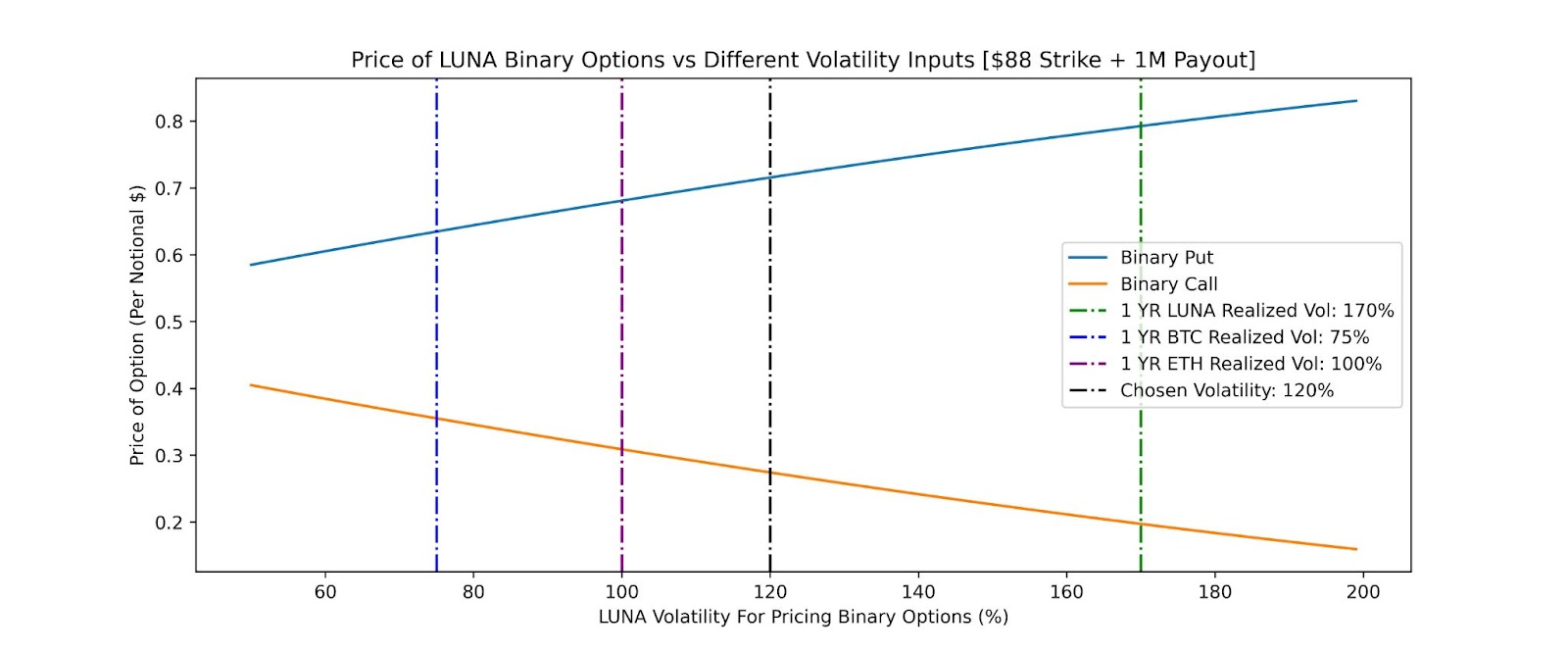

However, traders will have varying opinions on where LUNA volatility may be trading 1 year from now. At the time of this bet, 1 year LUNA realized volatility was trading at ~170%. Currently LUNA has established itself as one of the largest blockchains aside from Ethereum. As such, over the coming year, it’s reasonable to expect LUNA to become more of an institutionalized asset causing its volatility to fall relative to smaller market-capitalization protocols. In this view of the world, it’s reasonable to expect LUNA’s price volatility to be lower than 170% by March 2023.

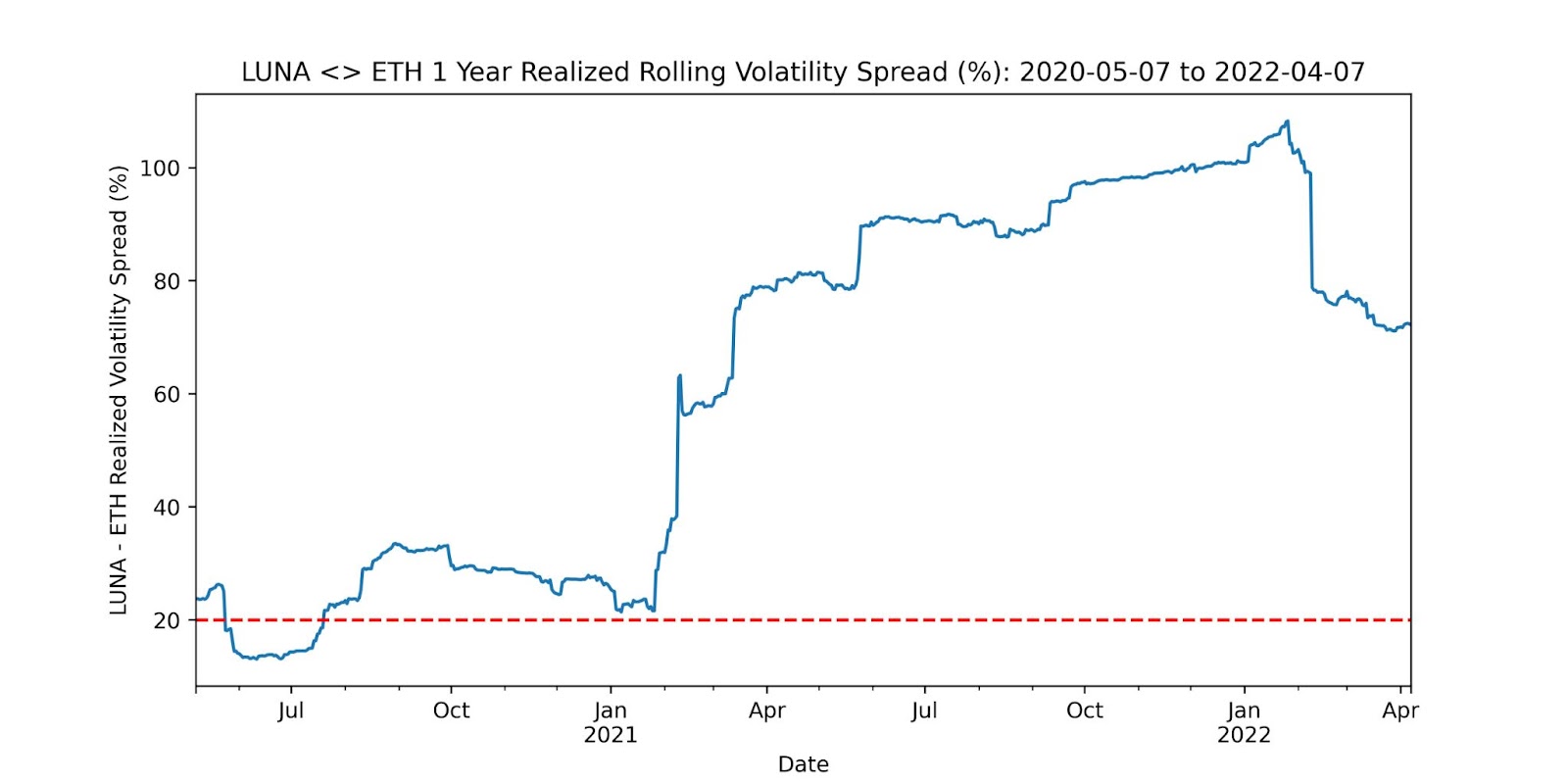

Given there is no publicly listed options market for LUNA yet, in these cases market-makers will use the ETH volatility surface as a proxy to bootstrap option markets on new assets. A starting point to approximate a fair volatility figure could be to analyze the historical 1 year realized volatility spread between ETH and LUNA as shown below.

We can see the realized volatility spread between LUNA and ETH was at its lowest for the latter half of 2020, ranging between 15 to 35 volatility points. In this case we can use 20 volatility points as an approximation for the spread we’ll add on top of ETH realized volatility to price out these binary options. At the time of the trade, 1 year ETH realized volatility was around 100% so our approximate 1 year LUNA volatility will be 120%. Given these are at-the-money strikes we won’t factor in any skew for the call and put volatility input (if the chosen strikes were farther away from $88 then we’d have to be more mindful of adding some skew to the volatility inputs used).

Based on a 120% volatility input, for each notional dollar, the value of the call is worth ~$0.30 and the value of the put is ~$0.70. However, given the cash payouts for this trade are the same, each party effectively entered into a 50/50 bet where Do bought a binary call for $0.50 and Algod bought a binary put option for $0.50. In other words, Do effectively “bought” a call option for $0.50 but its fair value is worth only $0.30. Furthermore, Algod received the put option for $0.50 when it’s theoretically valued at nearly $0.70.

To make this trade “fair” at inception, each leg of the trade should have been valued close to $0.50 per notional dollar. This could have been achieved by varying the inputs of the pricing model as shown below:

- Alternative 1: All else equal from the original bet, adjusting the strike price to $45 instead of $88 would have resulted in both the calls and puts trading for $0.50. Ie:

If LUNA > $45: Do gets paid $1M

If LUNA < $45: Algod gets paid $1M

- Alternative 2: All else equal from the original bet, adjusting the cash payouts for both Algod and Do can help bring the fair value of the options closer to $0.50. In this case Algod’s payout would have to be reduced from $1M to ~$750k and Do’s payout would have to be increased from $1M to ~$2M. ie :

If LUNA > $88: Do gets paid $2M

If LUNA < $88: Algod gets paid $750k

From this analysis we can tell the initial structure of this trade greatly favored Algod, however, this largely depends on the volatility assumed to price the options. Below we can see how the price of these binaries vary when using different volatility figures. Unlike what we observe with vanilla options, a higher volatility figure decreases the value of the call but increases the price of the put. With binary calls, even though the underlying asset price can theoretically go to infinity, the option payoff is limited to the fixed cash payout. As a result, with extremely high volatility even if this increases the probability of outcomes where LUNA is well above the call strike, this is not relevant for binary call options as the payoff would be capped. Rather, due to the nature of the log-normal distribution, extreme volatility would lead to more cases where the price could fall below the call strike, hence reducing the call price and increasing the put price.

As of today based on current market prices, both Algod and Do’s positions are still worth nearly the same since they both entered into this bet. However, we can shock the spot price input to see how the value of the binary call or put changes with respect to changes in LUNA’s price. Currently LUNA is trading for $100, however, if it pumped to $175 overnight then Do and Algod’s positions would be worth roughly the same amount.

Overall, to make this trade “fair”, each individual should have adjusted the cash payout and/or strike level to ensure the fair-values of the binary options are equal at inception. The moral of this story is to never agree to a 50/50 binary bet on altcoins with high volatility until you can determine the fair value of each leg. Although the expected payout may be equal on either side ($1M in this case), because the price can go up exponentially, the probability of LUNA going up also has to be proportionally lower to make the bet fair.

3. Backtesting LUNA Binary Option Trading Strategies

As an aside from the wager, in this section we’ll take some inspiration from the recent success of DeFi option vaults (DOVs) and backtest the historical performance of systematically trading LUNA binary call options. Given the limited price history for LUNA (only goes back since 2019), backtesting a 1 year maturity option strategy won’t provide us with too many data points. Rather, we’ll focus on shorter maturities such as weekly binary options. Furthermore, these short-term strategies may be more relevant for DOVs seeking to provide new products to their users.

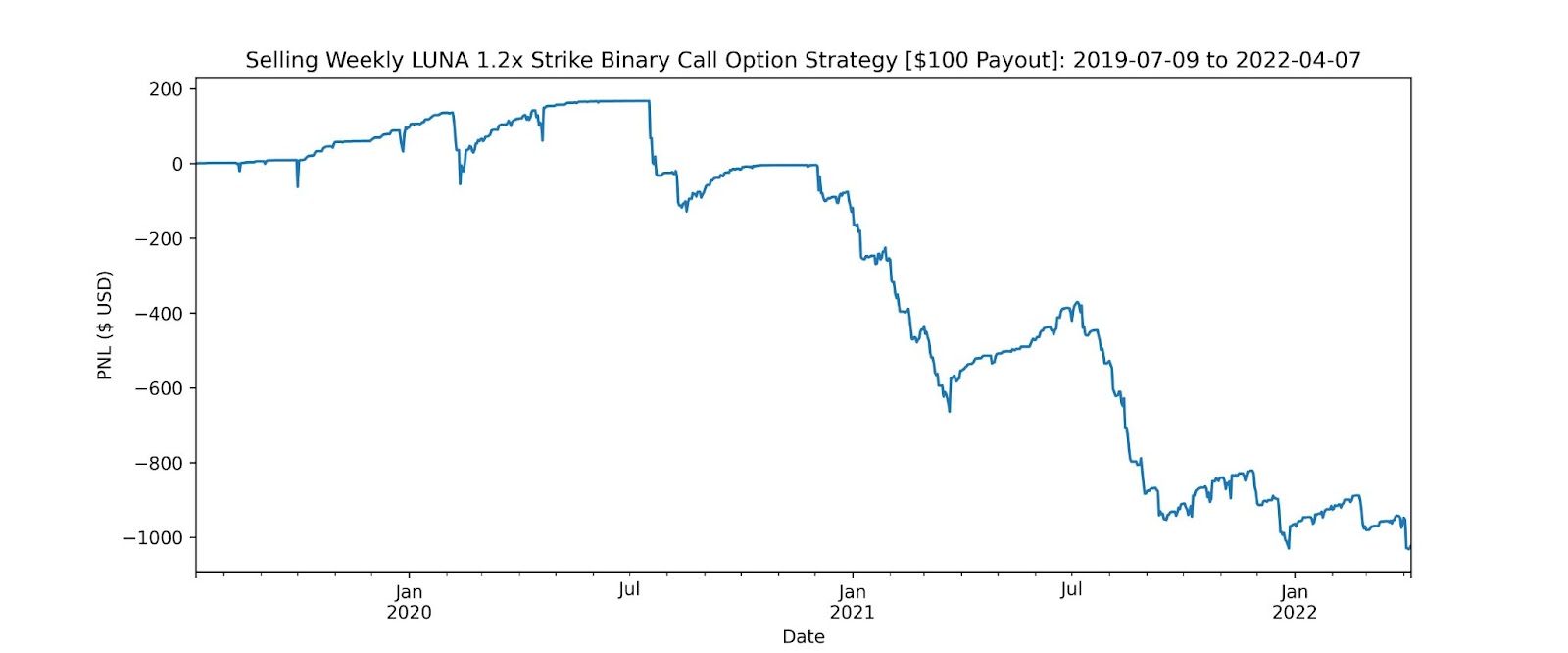

Let’s consider a scenario where the trader systematically sells a weekly binary call option with a strike price 20% above the LUNA price at the beginning of the week. Similar to vanilla options, these binaries are less impacted by volatility but more sensitive to the change in LUNA price. Therefore, we can keep things simple and model the P&L of systematically selling binaries with rolling 30 day volatility less a 15 volatility point spread. We apply this spread to reflect the edge option market-makers would want to capture relative to realized volatility when trading these options against a DOV. Lastly, we’ll specify the fixed cash payout to be $100 if the binary call option expires ITM.

To recap, every week the DOV will sell binary call options with a strike price 20% greater than the spot price of LUNA at the beginning of the week. This should give a sufficient margin of safety in the case of a massive pump in LUNA price (recall the DOV would face a fixed loss if the price of LUNA was above the strike price at expiry). As shown below this strategy does not generate positive returns as there were over 20 cases where LUNA jumped past the 20% strike threshold on a weekly basis.

We can also flip the model and backtest the P&L of systematically buying these binary call options on a weekly basis. For this backtest we have to add a 15 volatility point premium on top of 30 day realized rolling volatility to reflect the market-maker’s edge. In these cases we can see how the P&L is roughly the inverse of selling the LUNA binary options. There is a fair degree of theta decay from being long the options, however, the occasional periods of LUNA pumping past the call strike does produce a net positive return.

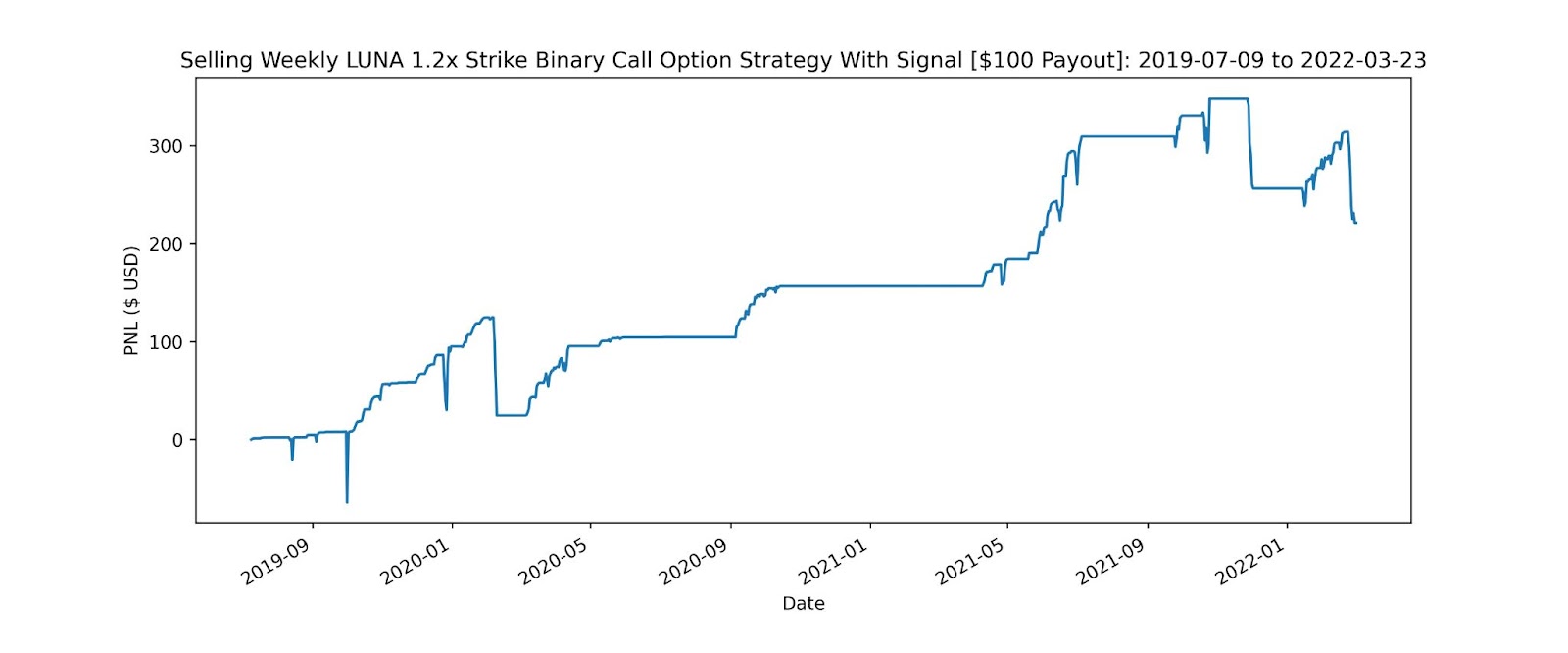

We can smooth out the PNL and improve the return profile for these strategies by including a simple trend signal to filter for ideal trading environments. In this case we’ll overlay a 7 day / 30 day simple moving average (SMA) and use the following logic:

- For call selling, only sell if the trend is bearish (ie: 7 day SMA < 30 day SMA)

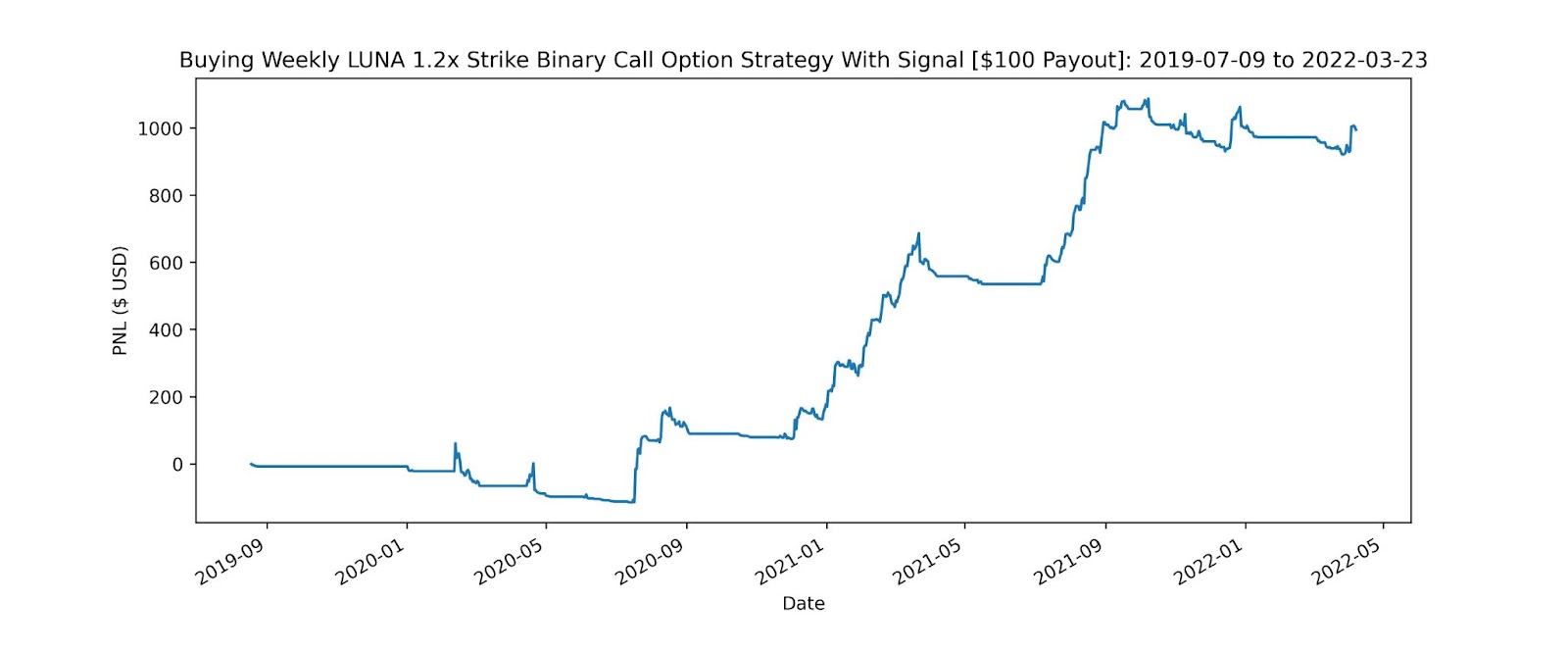

- For call buying, only buy if the trend is bullish (ie: 7 day SMA > 30 day SMA)

As shown below adding this simple filter to the systematic call selling greatly improves the overall returns. From a high level this makes sense because the model in theory would avoid selling calls during bullish regimes which reduces the chances of the binary option expiring ITM.

Furthermore, we can apply the similar logic to the call buying strategy. From a quick glance the returns appear to be similar, however, the addition of the trend filter appears to reduce volatility and smoothen out returns.

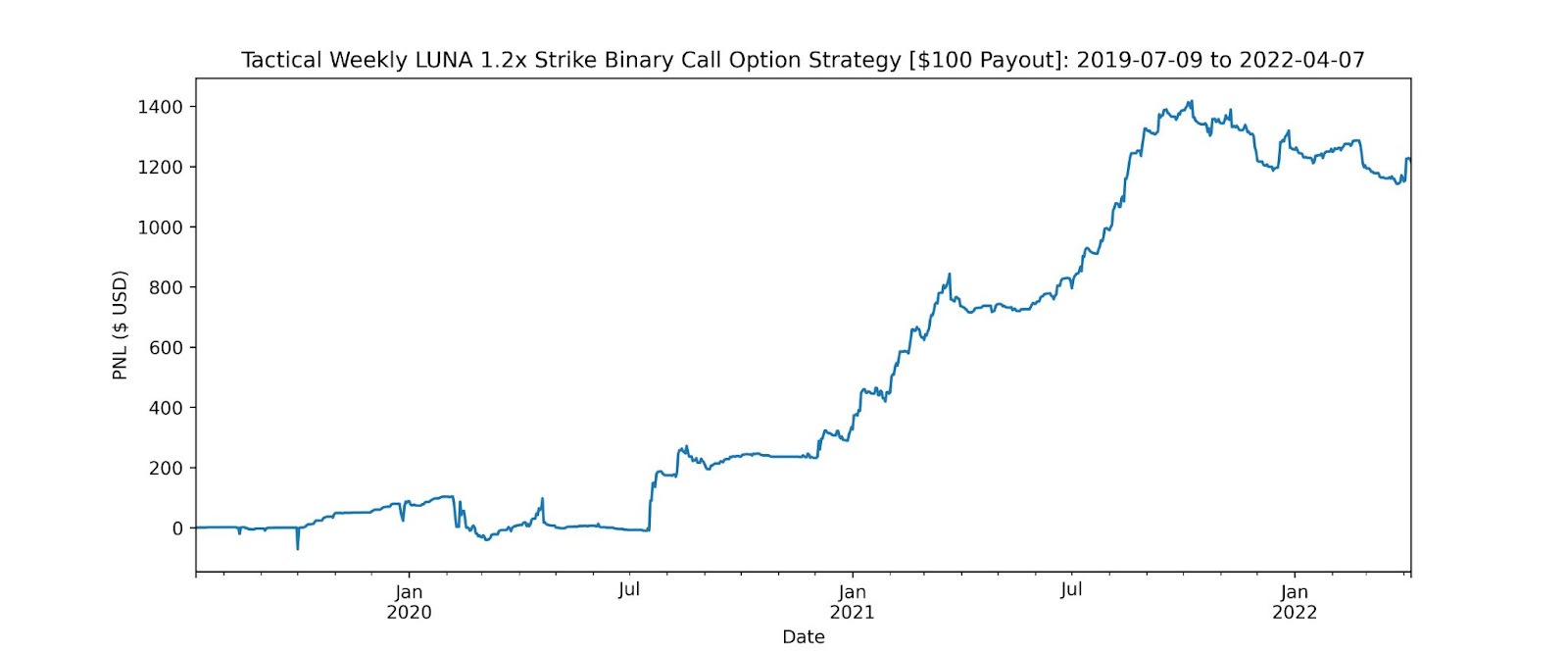

Lastly, we can take it one step further and combine the buying and selling of digital call options into a single strategy. This smooths out the return profile even further and results in higher overall absolute returns.

In our view as the DeFi options space continues to grow, we expect to see teams include more sophisticated strategies aside from systematically selling vanilla options. While these basic strategies are good starting points to attract users and grow TVL, in the long-run users will demand strategies which provide sustainable returns during changing market conditions. As demonstrated above, in many cases it only takes small adjustments to a naive strategy to drastically improve the overall risk-adjusted returns and thereby offer better yields to users.

Thinking Ahead...

While this research piece does not dive into the LUNA and UST debate we can say that Do is a visionary builder and has created a unique demand for UST aside from purely financial reasons. The growing real-world demand for UST such as with the Chai app in South Korea showcases UST’s competitive advantage compared to existing algorithmic stablecoins. However, at the same time many investors have questioned the reliability of Anchor Protocol’s deposit yield which has been a significant driver for UST growth and subsequently the appreciation of LUNA. If the advertised yield on Anchor were to fall below a certain threshold this could reduce demand for UST to be deposited into Anchor and subsequently cause pressure on LUNA’s price. Furthermore, the price of LUNA is not immune to risk-on events so despite everything else going right on a protocol level, a black-swan macro event could cause LUNA to plummet (alongside the broader crypto market).

Regardless of the outcome in a year, this bet can inspire builders to work on new financial derivatives within the DeFi ecosystem. Furthermore, DOVs may wish to move beyond vanilla options and explore exotic options strategies as demonstrated in the trend-following binary trading strategy. Cega Protocol is a project working on providing DeFi users with sustainable yield by using exotic option structures. We believe projects like these will help push the boundaries of the current DeFi derivatives ecosystem while making it easier for degen traders to make bets like these in the future.

Acknowledgements: Sohan Sen and Shiliang Tang for explaining the mechanics of how binary options work and proof-reading this piece. Shoutout to Lily Francis for the initial analysis which formed the basis for this research piece.

Disclaimer: Nothing mentioned in this article constitutes as financial advice. LedgerPrime is an investor in Cega. Opinions expressed are solely my own and do not express the views or opinions of LedgerPrime